Netherlands vs. China: How the Nexperia Standoff Is Repricing Power Discretes

At a Glance

Analyze how the Nexperia standoff impacts power discretes pricing. Discover why geopolitical risk is driving availability issues and procurement gaps.

For years, power discretes have been one of the least challenging parts of sourcing, with balanced supply, controlled pricing, and trusted supplier contracts.

That assumption is starting to break.

The Nexperia standoff has added a geopolitical risk premium to even the most common components. Spot prices are rising, contract prices are lagging, and availability is no longer guaranteed.

Automotive and industrial players are already feeling the impact, and the pressure is starting to move into broader IC categories. If export controls tighten further, this won’t be a short-term disruption. It will reshape how risk is priced across the semiconductor supply chain.

Key Takeaways

- The Nexperia situation has introduced a geopolitical risk premium into even the most commoditized components.

- Spot pricing leads while contracts lag, creating widening procurement gaps.

- Automotive and industrial buyers are the first to bear the impact, constrained by long qualification cycles and limited flexibility in supplier switching.

- Disruption at Nexperia is no longer a single-supplier issue; it’s already spilling into analog, MCU, memory, and passive components, signaling broader market repricing ahead.

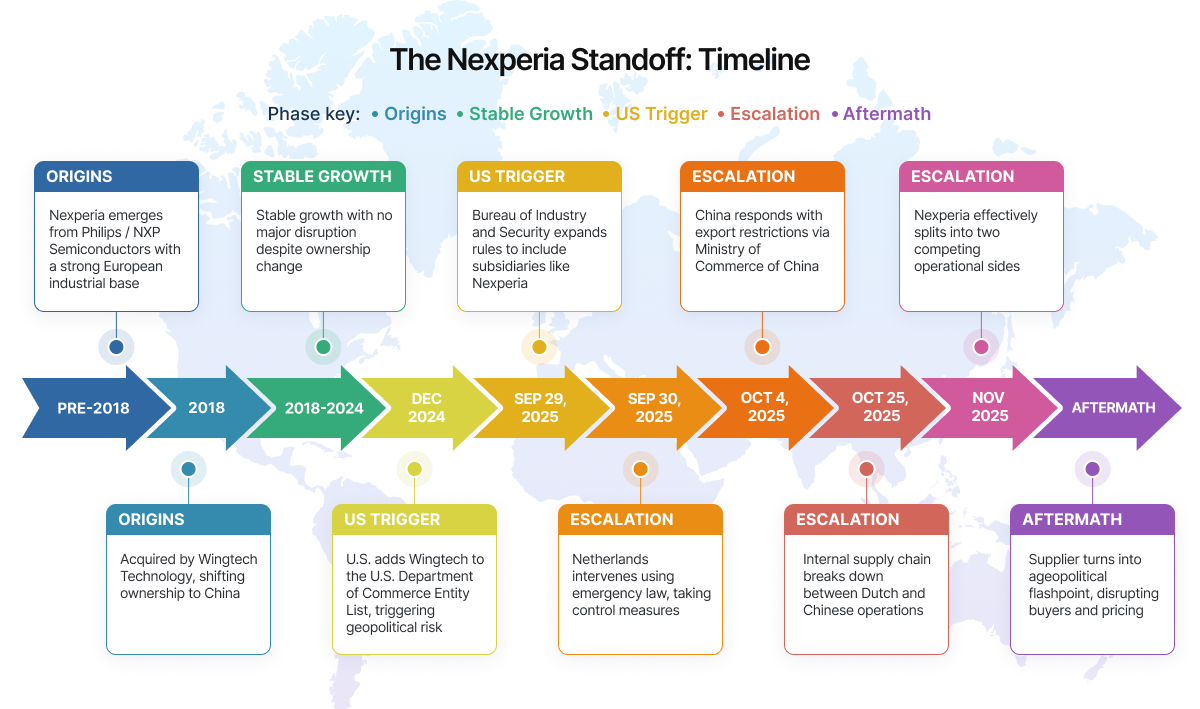

What Happened: A Timeline of the Standoff

To understand the pricing shift, you need to look at how quickly a relatively stable supplier became a geopolitical risk event.

Nexperia was once part of Philips and later NXP, giving it a strong European industrial identity. In 2018, it was acquired by China’s Wingtech Technology, placing it under a Chinese-controlled group. For several years, this ownership change didn’t materially disrupt operations.

Nexperia continued to grow, reaching $2.06 billion in revenue by 2024, expanding market share from 8.9% to 9.7%, with around 60% of that revenue coming from automotive customers.

The situation shifted when U.S. policy stepped in.

- December 2024 - The U.S. adds Wingtech to its Entity List, raising concerns about China’s semiconductor growth.

- September 29, 2025 - The Bureau of Industry and Security expanded export rules to include companies owned by listed firms, directly affecting Nexperia.

- September 30, 2025 - The Netherlands reacted quickly, stopping wafer shipments to China.

- October 4, 2025 - China responds with export controls on certain components and sub-assemblies

From that point, the split became operational. By early November, the company was effectively divided against itself. What had been a single, integrated supplier was now two sides acting independently, creating confusion and supply challenges for automotive and industrial buyers.

How Stable Supply Becomes Unpredictable Overnight

If you’ve been managing sourcing over the past few months, this situation will feel familiar. You’re working with a stable design, qualified components, and a supplier like Nexperia that’s been reliable for years. Pricing is predictable. Lead times are manageable. Nothing feels risky. And suddenly, everything starts to move because of the Nexperia standoff.

- RFQs stop behaving normally: You send out requests expecting routine quotes. Responses come back, but something’s off. Stock is limited and validity periods are shorter, sometimes just hours. You hesitate, thinking you’ll confirm internally first.

- What you’re quoted isn’t what you’ll pay: You return to place the order, and the price has already moved. Not slightly, but enough to trigger a new approval cycle. What used to be a simple PO now needs escalation.

- Purchasing without full visibility: Production timelines don’t wait. You approve the higher price, place the PO, and then the response comes: “stock no longer available.”

- Availability becomes competitive: Supply still exists, but it’s no longer evenly accessible. Allocation depends on speed and price. Buyers aren’t just sourcing anymore, they're competing.

Inside the team, pressure builds quickly:

- Buyers keep refreshing quotes, trying to secure stock before it moves again.

- Engineers are pushed to find alternates but validation cycles don’t compress easily.

- Planning teams try to schedule production with inputs that change daily.

Even when engineers qualify an alternate, it doesn’t fully solve the problem, because the entire market is shifting at the same time. That alternate supplier, once a backup, suddenly becomes the new bottleneck. Lead times stretch. Capacity tightens. Prices also start climbing.

What begins as a supplier-specific disruption turns into a broader market problem. And the hardest part? Nothing breaks all at once. It’s a series of small changes that add up to constant pressure.

The Geopolitical Risk Premium: How It Shows Up in Pricing

The most immediate impact of the standoff isn’t making headlines; it's showing up in pricing behavior.

Power discretes were traditionally priced on manufacturing economics: wafer costs, fab utilization, and demand cycles. That model is no longer sufficient. Pricing now reflects uncertainty.

What buyers are paying for has changed. It’s no longer just availability but the risk of what happens next.

Here’s how geopolitical premium is showing up in practice:

1. Spot Price Inflation

Distributors and brokers are raising spot prices even when stock is available. Parts linked to exposed supply chains are being quoted 5-15% higher, with some automotive-grade components quoted at over 20%. The premium reflects anticipated disruption, not actual shortage.

2. Wider Spreads vs. Contract Pricing

A growing supply-demand gap estimated at around 3.2% is pushing the market toward longer, more predictable contracts. But long-term agreements are lagging behind real-time market shifts, creating a widening gap between what procurement teams expected to pay and what they are being quoted for immediate shortages.

3. Inventory Hoarding Behavior

Some buyers are building safety stock, effectively pulling demand forward. This tightens availability and drives costs higher. What makes this cycle different is that it’s driven not only by supply and demand but also by expectations. The market is reacting to what could happen next, not just current conditions.

4. Regional Price Divergence

The same component is now priced differently across regions, depending on trade restrictions, logistical friction, and perceived supply risk.

In practice, the geopolitical premium isn’t a separate line item. It’s embedded in every quote, negotiation, and sourcing decision.

That’s where platforms like Octopart add value in this environment, offering visibility not just into pricing, but into regional differences and availability.

Who's Absorbing the Shock First

The initial impact is not evenly distributed. Some sectors are exposed earlier and more heavily than others.

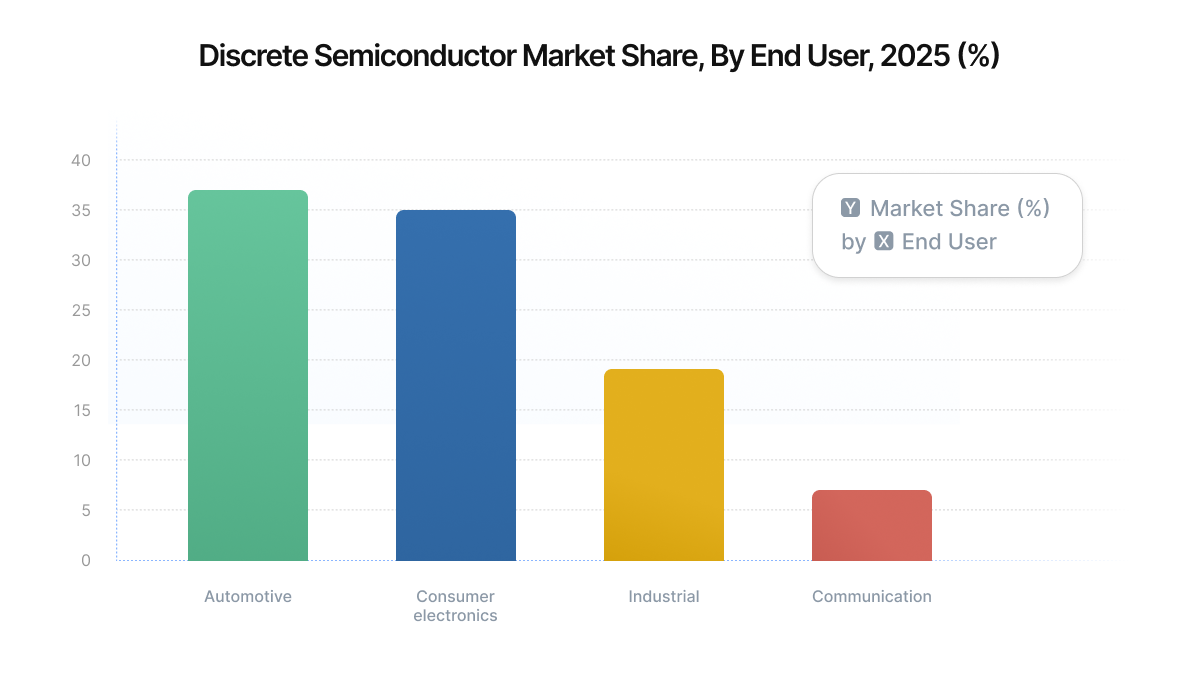

- Automotive OEMs and Tier 1 suppliers: Automotive remains one of the largest consumers of discrete semiconductors, accounting for around 37% of discrete semiconductor demand, and continues to grow with EV and electrification trends. Automotive qualification cycles often take 6-12 months, making rapid supplier switching difficult. As a result, automotive buyers are absorbing higher costs rather than risking production delays.

- Industrial equipment manufacturers: Industrial systems, including motor drives, power supplies, and factory automation, rely heavily on high-volume discrete components. These buyers are more flexible than automotive, but still face constraints due to design dependencies and certification requirements.

- Contract manufacturers (EMS): EMS providers sit between supplier volatility and fixed customer pricing. They are often forced to procure at elevated spot prices while honoring fixed-price contracts downstream.

- Smaller OEMs and startups: These players are the most exposed. Without long-term agreements or strong supplier relationships, they are pushed directly into the spot market, where volatility is highest.

Ripple Effects Into Broader Commodity ICs

What starts in power discretes doesn’t stay contained. As supply tightens and pricing pressure builds around players like Nexperia, the impact is now spreading across the wider component ecosystem.

This pressure is now visible across the following segments:

Analog ICs (TI) are already seeing broad repricing, with increases typically in the 10-30% range.

Analog ICs (ADI) are following a similar path, with average increases around 15%, with several parts reaching up to 30%.

MCU / Logic suppliers are entering early pricing cycles, especially in automotive, with hikes reaching between 15-50%, especially in automotive-grade components.

Memory markets are tightening, with spot prices jumping over 300%, as capacity shifts toward AI-driven demand.

Discretes are seeing extended lead times, now stretching 6-8 weeks, particularly impacting automotive and industrial demand.

Packaging / passives are under cost pressure, as metals and OSAT costs rise sharply 60-80%.

What Happens If Export Controls Tighten or Governance Remains Split?

If export controls tighten further or governance remains split, components that are technically available may become commercially inaccessible.

Lead times could extend not because of capacity constraints, but because of compliance checks, documentation requirements, or shipment delays. In some cases, the same part number could require different approvals depending on where it was fabricated or assembled.

- Approved suppliers may no longer be usable across all regions.

- Inventory at one site may not be transferable to another.

- Procurement cycles slow down as compliance becomes part of sourcing.

- Pricing becomes less predictable and more region-specific.

Final Takeaway

The Nexperia situation is a reminder that even the most commoditized components are no longer insulated from geopolitics. Power discretes may not grab the same attention as advanced nodes or AI chips, but their importance and exposure are just as real.

For engineering and procurement teams, the takeaway is clear: pricing is no longer driven solely by cost and demand. It’s shaped by risk. And increasingly, that risk is geopolitical.

About Author

Related Resources

Related Technical Documentation

Table of Contents

- Key Takeaways

- What Happened: A Timeline of the Standoff

- How Stable Supply Becomes Unpredictable Overnight

- The Geopolitical Risk Premium: How It Shows Up in Pricing

- 1. Spot Price Inflation

- 2. Wider Spreads vs. Contract Pricing

- 3. Inventory Hoarding Behavior

- 4. Regional Price Divergence

- Who's Absorbing the Shock First

- Ripple Effects Into Broader Commodity ICs

- What Happens If Export Controls Tighten or Governance Remains Split?

- Final Takeaway

Design to Release, Without the Friction

- Keep reviews tied to the right version

- Reduce handoff confusion and rework

- Spot sourcing and release risk earlier

- Work solo, share when needed

Get Started

Thank you, you are now subscribed to updates.