What the Nexperia Saga Teaches About Component Strategy

At a Glance

Learn what the Nexperia saga reveals about component strategy. Discover how to build resilient BOMs and avoid costly disruptions from supply chain risk.

It wasn't a cutting-edge processor. It wasn't a next-gen memory chip or an advanced AI accelerator. The component that nearly stopped Volkswagen's Wolfsburg plant, the world's largest automotive factory, from building Golf and Tiguan models in October 2025 was a diode. The kind of part that gets approved early, locked into the BOM, and rarely questioned again, because it’s cheap, standard, and widely available. Until the day it doesn't ship, and suddenly the most overlooked line item on the parts list becomes the reason an entire production line goes quiet.

That’s the real story behind the Nexperia saga that should stay with every engineer and procurement professional long after the headlines fade.

Because this wasn’t just a disruption. It was the moment a “commodity” part became a single point of failure, exposing how fragile most BOM strategies really are.

Key Takeaways

- Availability has moved beyond volume and standardization. If resilience isn’t designed into the BOM, a single policy decision can disrupt entire production lines.

- Dual footprints, pre-qualified alternates, and wider parametric ranges need to be built in upfront to create flexibility.

- Multi-region agreements and safety stock near the final assembly can matter just as much as the silicon selection.

- Export controls and regulatory shifts should be treated as core supply parameters evaluated alongside lead time, cost, and MOQ to avoid hidden risk.

Most BOMs are built to optimize three factors: cost, performance, and availability. On paper, that’s enough to move a design from prototype to production.

In reality, the Nexperia situation introduced a fourth factor that most BOMs simply don’t account for:

Governance risk.

- Who controls the supply?

- Where is it manufactured?

- What political decisions can interrupt it overnight?

If those questions aren’t part of your component selection, then your BOM is exposed.

Industry projections point to a global semiconductor market approaching $1 trillion by 2026 with growth across multiple regions. However, that growth is increasingly concentrated. What looks like a global scale is, in reality, tightly coupled dependence.

In Nexperia’s case, the risk was amplified by its heavy reliance on China. Around 70% of its chips are packaged and distributed in China, with only about 30% split between Malaysia and the Philippines.

Regional Revenue (US$M)

|

Region |

2024 |

2025 |

2026 |

YoY 2024 |

YoY 2025 |

YoY 2026 |

|

Americas |

195,123 |

251,926 |

338,574 |

+45.2% |

+29.1% |

+34.4% |

|

Europe |

51,250 |

54,127 |

60,429 |

−8.1% |

+5.6% |

+11.6% |

|

Japan |

46,739 |

44,835 |

50,164 |

0.0% |

−4.1% |

+11.9% |

|

Asia Pacific |

337,437 |

421,354 |

526,293 |

+16.4% |

+24.9% |

+24.9% |

|

Total World |

630,549 |

772,243 |

975,460 |

+19.7% |

+22.5% |

+26.3% |

Closing that gap requires three structural changes in how components are selected, validated, and sourced.

Resilience Starts in the BOM, Not in Last-Minute Sourcing Decisions

The cheapest moment to build resilience into a product is during design. Once a schematic is frozen and layout is complete, flexibility becomes expensive. Changes mean respins, requalification, and certification delays.

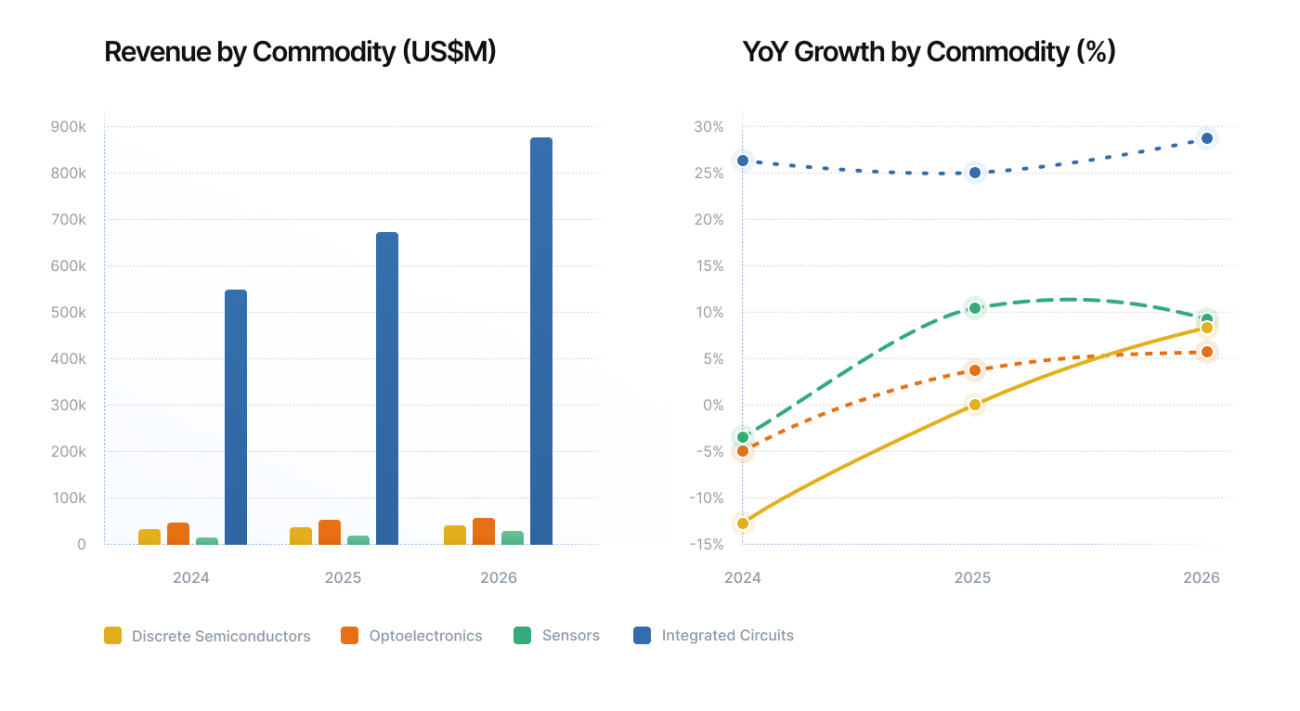

The chart showing discrete semiconductors as nearly invisible next to integrated circuits explains why low-value components are often overlooked in BOM design. They're a rounding error in revenue terms, but they have an outsized impact in real-world disruptions.

Below are the design strategies that turn this overlooked risk into built-in resilience.

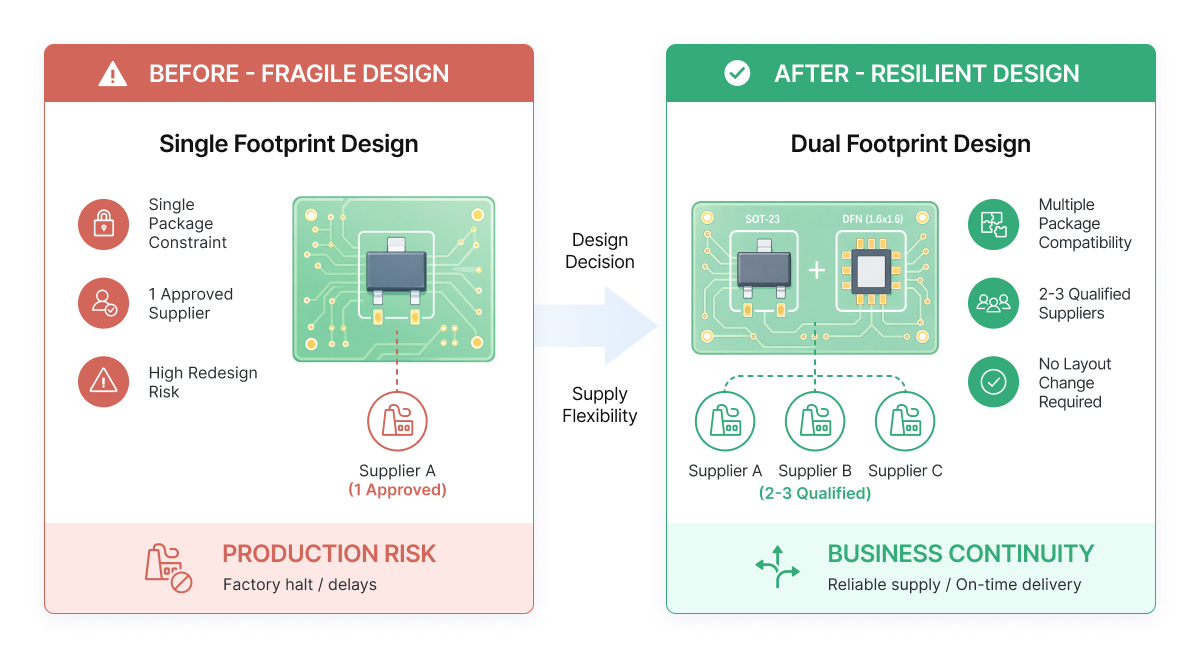

1. Dual Footprints as a Baseline, Not an Exception

Designing around a single package or pin configuration quietly limits your supplier options. When disruption hits, that constraint turns into costly redesign cycles.

Dual footprints remove that fragility, giving engineers the flexibility to support multiple package options from the start.

Common footprints like SOT-23, TO-252, or DFN can often support equivalent parts across multiple manufacturers without layout changes. Procurement teams can switch sources quickly without waiting on engineering change orders, keeping lines running without delays.

2. Flexible Parametric Guardrails

Engineering teams often lock in tight parametric ranges, sometimes tighter than the application truly requires. That works in stable conditions, but in a constrained market, it quickly becomes a sourcing bottleneck.

Specifying a MOSFET with ±5% Rds(on) tolerance when the design would comfortably operate at ±10% can limit your sourcing options. Define parameters based on actual circuit requirements, not initial simulation, and clearly document acceptable ranges so sourcing teams can move quickly on alternates.

3. Pre-Qualified Alternates

When component shortages hit, parts sourced from the open markets can cost 200-300% above standard rates. Industry research shows that building an AVL with 2-3 second sources cuts shortage delays by 80%.

Alternates should be identified and locked in during the design phase:

- Select 2-3 viable alternatives

- Validate them under real operating conditions

- Document interchangeability in the BOM

Prioritize where the risk is highest:

- Single-sourced components

- Long lead-time parts (>16 weeks)

- Suppliers with geopolitical exposure

At scale, this only works with the right data. Platforms like Octopart enable teams to pre-identify alternates using parametric search across thousands of distributors, with up-to-date visibility into stock, pricing, and lead times across multiple regions.

Instead of scrambling in a crisis, teams can act on validated parts already tested and documented in the BOM.

Commercial Levers Matter as Much as Silicon Choices

Having alternate parts isn’t enough if your commercial structures are still concentrated. The Nexperia situation highlighted how it can quietly amplify disruption instead of absorbing it. To actually build resilience, three commercial levers need to be designed with the same intent as your component choices:

1. Multi-Region Framework Agreements

You are not diversified just because you have multiple suppliers on paper. Multiple suppliers don’t help when contracts, manufacturing, and logistics are tied to the same concentrated regions.

Multi-region frameworks reduce that exposure. Here’s what to look at:

- Concentration Check: Is more than 60-70% of volume dependent on one region or legal entity? If yes, you have a structural risk.

- Avoid Single Legal Entity Dependence: Even within one supplier, structure contracts through different regional entities where possible to reduce exposure.

- Split Contracts by Region: Don’t rely on a single global agreement. Create parallel contracts across at least two regions (e.g., North America + Europe or Europe + Asia).

- Pre-Allocate Volume Across Regions: Don’t keep alternates as theoretical. Assign a percentage of forecast demand to each region so relationships and supply lanes stay active.

- Build Logistics Redundancy: Qualify multiple shipping lanes and partners. A contract without a viable logistics path is still a single point of failure.

This doesn’t eliminate risk, but it prevents a single policy decision from shutting down your entire production line.

2. Safety Stock Near Final Assembly

Lean inventory holds up in stable conditions. Under pressure, it becomes a weak point.

Strategic safety stock, especially positioned near final assembly, acts as a buffer:

A practical baseline looks like:

- 8-week buffer - For high-running assemblies and long lead-time parts

- 12-week buffer - For components with unique footprints, long qualification cycles, and regionally concentrated supply.

On paper, a 12-week buffer in a bonded warehouse near your contract manufacturer looks costly, however, in reality, it’s far cheaper than an eight-week line stoppage while you qualify an alternate and chase allocation.

This isn’t excess inventory. It’s about holding the right inventory where it provides maximum protection with minimal capital impact.

Treat Governance Risk as a Supply Parameter

What once sat outside the supply chain now sits at its core. Governance risk has become a primary driver of component flow and availability, operating like any other supply parameter.

Supplier ownership, regulatory pressure, and geopolitical alignment are directly shaping availability, pricing, and continuity, just like lead times or capacity.

And like any other parameter, it needs to be evaluated, monitored, and incorporated into decision-making.

Key areas to focus on:

- Include Governance in Part Selection: Evaluate supplier ownership, region of control, and regulatory exposure alongside price, performance, and availability.

- Continuously Monitor Policy Signals: Track export controls, trade actions, and regulatory developments that could impact component flow.

- Map Inventory by Geography: Ensure visibility into where stock physically sits, not just total availability. Regional buffers matter more than global numbers during disruption.

- Flag High-Exposure Components: Tag parts where governance risk could impact continuity, even if current supply looks stable.

This isn’t about predicting policy decisions but ensuring that one decision doesn’t stop your supply chain.

What This Means for Cross-Functional Teams

For Systems Engineers

- Design with flexibility from the start

- Challenge overly tight specifications

- Validate alternates for real-world performance, not just datasheet-level compatibility

For Engineering Leaders

- Build processes that support the pre-qualification of alternates

- Integrate supply risk into design reviews

- Balance performance optimization with resilience requirements

For Procurement Teams

- Structure sourcing strategies with geopolitical exposure in mind

- Maintain visibility into both contract and spot markets

- Collaborate early with engineering to influence component decisions

When these functions align early, resilience stops being reactive and becomes a built-in advantage across the entire product lifecycle.

Final Takeaway

Resilience is no longer a sourcing tactic but a design decision. The Nexperia saga showed how even the most overlooked components can become critical failure points when flexibility isn’t built in early.

BOMs optimized only for cost and performance are inherently fragile in a world shaped by geopolitical shifts and regulatory pressure. The teams that stay operational will be the ones that think beyond immediate requirements and design for uncertainty.

Dual footprints, validated alternates, diversified supply, and governance awareness are part of the design. The difference isn’t in how teams respond to disruption, but in whether their designs leave them exposed to it in the first place.

About Author

Related Resources

Related Technical Documentation

Table of Contents

Design to Release, Without the Friction

- Keep reviews tied to the right version

- Reduce handoff confusion and rework

- Spot sourcing and release risk earlier

- Work solo, share when needed

Get Started

Thank you, you are now subscribed to updates.